Since peaking at over $200 a share in February, Universal Display��s (OLED) gave the stock a lift back to over $100 share but even that rally faded. If EPS (earnings per share) growth will top 85 percent next year, implying a 27.7 times forward P/E, and 32.6 percent annually over the next five years, will OLED stock trade back at the 50 times forward earnings multiples, or $200 a share, anytime soon?

Management revised its 2018 revenue guidance to between $280 million and $310 million. In terms of materials sales, it believes the first quarter is a ��bottom�� for the year. At first, OLED stock slumped after the downside guidance, since expectations for ��significant�� growth in OLED panel demand failed to assure investors. In the near-term, the company still expects weak OLED panel demand due to the soft smartphone environment. This echoes the outlook of that of Samsung and LG.

OLED data by YCharts

OLED data by YCharts

Universal��s forecast of OLED growth, not in financial terms but in measures, is puzzling. The company could be avoiding the real headwinds from Apple Inc.(AAPL) using LED displays to lower costs. This poses a business challenge for Universal Display because a shift away from OLED would end the rich royalties the company currently enjoys. The company said:

Looking out for 2019, we anticipate the significant growth in the OLED industry to resume, as we expect the installed capacity base as measured in square meters to increase by approximately 50% by the end of 2019, as compared to the end of 2017.

Source: SA Transcript

The company must now pin its revenue growth in 2019 to LG Display��s (LPL) OLED TVs. Investors of Himax Technologies (HIMX) will already know that OLED and 8K televisions could drive television sales in the future. In its conference call, Himax said:

TV makers are rushing to develop super high-end products with 8K resolution. I am pleased to report that our team has recently secured another 8K TV design win for a major panel maker and expect more to come in the next few quarters. We expect a low-single-digit sequential revenue growth for large display driver ICs, a double-digit growth year-over-year.

Source: SA Transcript

HIMX data by YCharts

HIMX data by YCharts

Even though both stocks priced in the potential in sales stemming from OLED or 8K televisions, Himax is a more diversified company with a market capitalization of just $1.24 billion. OLED stock is valued at fourfold times more, leaving it little room to disappoint investors.

Despite the unknowns Universal Display faces, the smartphone refresh from Sharp, using Gen4 panels and BOE technology ramping up the use of Gen6 flexible OLED will give the company some booked sales for next year. BOE invested $7.3 billion in the plant and is committed in delivering devices having OLED displays.

China is another region whose fragmented Android market will not deter suppliers in building devices having OLED display.

Growth in AutomotiveThe rise in autonomous automobiles and infotainment created more demand per vehicle for technology components. Ambarella (AMBA) will benefit from CV1 (computer vision) sales to car suppliers. Intel (INTC) already expects billions in sales thanks to Mobileye. Nvidia (NVDA) DRIVE testing continues in artificial environments. For Universal Display, the company has an addressable market of just $4 million in automotive OLED display today. By 2022, the TAM (total addressable market) is $5 billion.

Near-term RisksInvestors are demanding more than the promise of potential revenue next year or by 2022. Near-term risks are higher than average. In the first quarter, premium smartphone demand weakened, causing OLED panel demand to fall. Total material sales fell to $25.3 million, compared to $46.6 million last year. Green/Yellow emitter sales totaled $17 million, compared to $33 million last year. EPS of $0.13 is down from $0.22 last year.

Cheap LED DisplaysOLED stock is pricing in the potential competition from smartphone makers like Apple using cheaper LED displays. But if OLED is more efficient with power, is more cost-efficient and offers better performance, smartphone makers cannot afford to leave OLED out. Conversely, if premium phone demands continue to weaken, smartphone designers must cut component prices drastically to drive demand. Universal Display would need to dramatically cut prices by lowering its royalty rates.

Valuation and TakeawayUniversal Display is very unlikely to re-visit $200 any time soon. Investors irrationally mispriced the stock in their belief that demand for premium, expensive smartphones would continue indefinitely. Though LED displays may replace OLED, the OLED technology is still a better choice. Prices must fall for OLED, so the price-earnings multiples on Universal Display stock may need to come down, too.

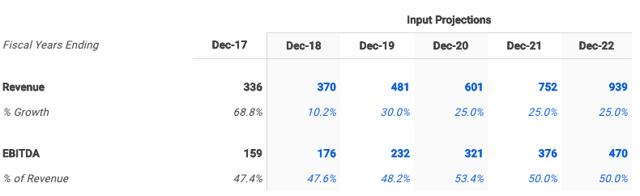

Of all the fair value models on OLED stock, which implies a price target of $89, a 5-year DCF Growth Exit model would suggest the stock already trades at a fair value at $97. This assumes that revenue grows in the range of 10 percent to 30 percent over the nex t five years.

Source: finbox.io (click on the link to change assumptions)

Please [+]Follow me for value stocks on sale. Click on the big "follow" button beside my avatar.

Disclosure: I am/we are long HIMX.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

No comments:

Post a Comment